Accounting for crypto – is change coming?

Crypto assets have long been a foreign concept to many in the finance world - explaining ‘blockchain’ and ‘cryptocurrencies’ in layman’s terms is no mean feat. The challenge many SMEs encounter with these types of asset is that the accounting treatment hasn’t caught up with the technology yet.

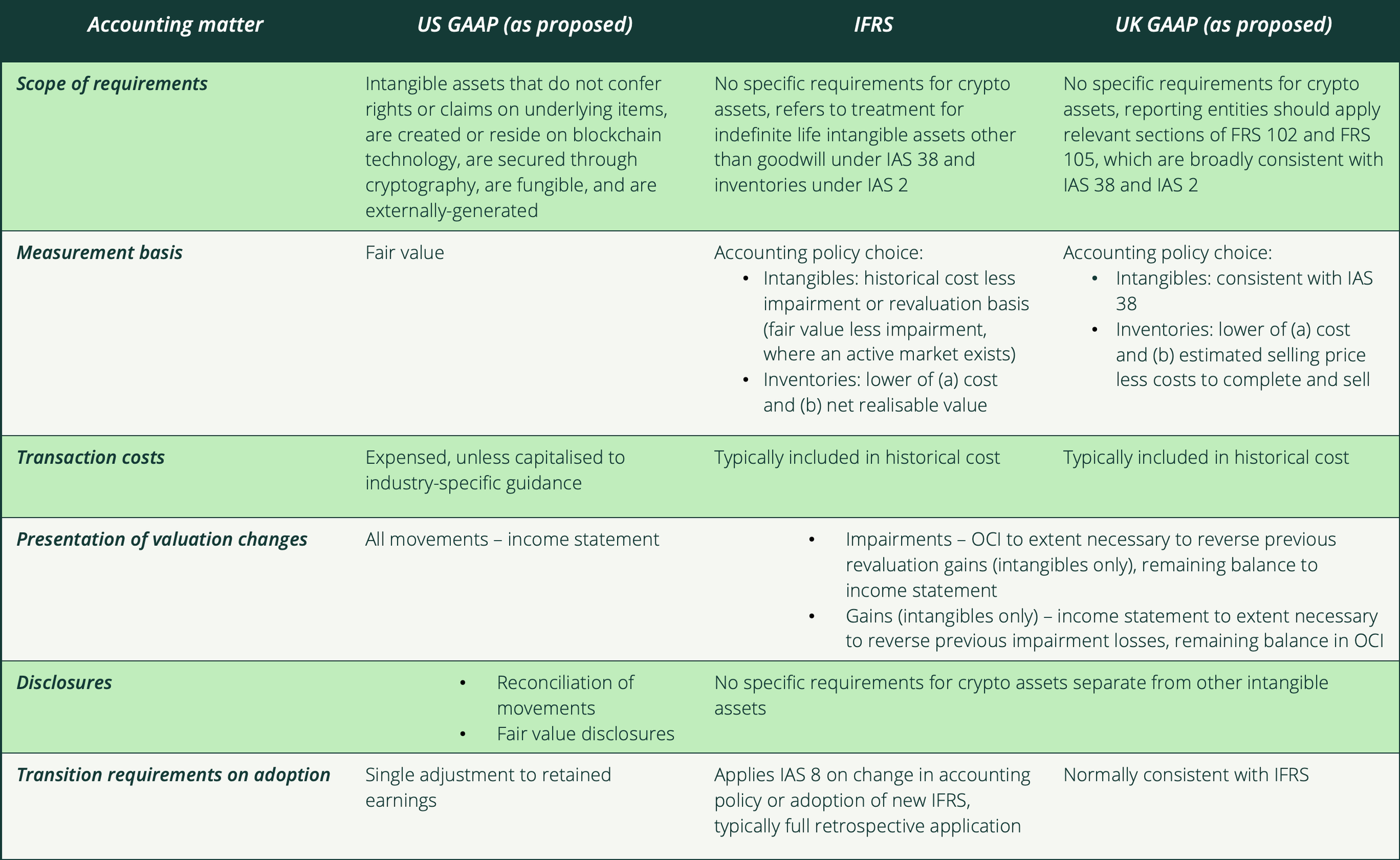

To put things into context, the most prevalent international requirements for ‘intangible assets other than goodwill’ are set out in IAS 38 Intangible Assets. (By ‘intangible assets other than goodwill’ we typically mean assets recognised on the balance sheet that do not have physical substance or a direct contractual entitlement to receive cash, and did not arise from a merger or a business acquisition – for example: customer lists, distribution agreements, and purchased intellectual property assets.) The trouble is that IAS 38 was issued in September 1999 – the same month that Google was born – and has not changed much since then. As a result, there can be considerable diversity in practice between companies in accounting for more complex intangibles such as crypto assets.

In March 2023, the Financial Accounting Standards Board (FASB) in the US (tasked with setting the accounting requirements for US groups and any companies reporting under US GAAP) issued its proposals specifically for crypto assets. The FASB’s international equivalents have been quieter than the Marie Celeste as far as the accounting treatment goes in this area, so the US have seized the initiative here.

Broadly speaking, Ancoram believes the FASB’s proposals are conceptually sound, although we have some concerns that some crypto assets such as NFTs are excluded from the scope. To find out more, you can download our response to the FASB here. In summary, the FASB has proposed:

Requiring crypto assets to be restated to market value at each interim or year end

Any unrealised gains or losses on crypto assets to be presented in P&L

Disclosing a reconciliation of movements in crypto asset valuations (in total), to demonstrate purchases, sales, revaluations and other movements

Disclosing information on ‘significant’ crypto asset holdings, including the name and type of crypto asset

The primary challenge with the FASB’s approach is that it is very different to requirements issued internationally by the IASB and in the UK by the Financial Reporting Council. Here’s a table summarising the key differences:

Ancoram specialises in accounting for highly complex transactions (as well as other reporting matters). Book a free consultation with our director, Tim Dee, if you think your business needs to optimise its accounting treatment of crypto assets under IFRS, UK or US GAAP. We work through the detail so you and your auditors can be confident of the result.